Birker2020

Well-Known Member

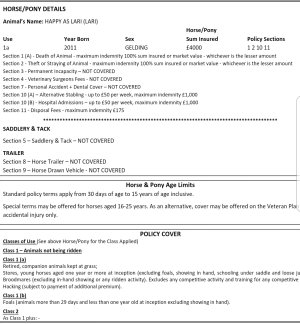

Wow SEIB have just rung me with my renewal and said its a premium of £600. This is for Lari insured for 10K value and no vets fees. Said I was thinking of cancelling it as he’s retired and not ridden anymore and I can’t justify paying £46 per month let alone £50 a month now its gone up again.

The lady said, ‘Oh we didn't realise he was retired, that will bring your premium down, and while we're here do you want to change his value so your premium will come down?”

So now he’s insured for destruction on humane grounds under BEVA guidelines, no vets fees. So now its £15 per month instead of £50 at a value of 4K! I have no idea how they determine value on a retired gelding but still. Stand more chance of getting that than 10K! I hope I never have to but nice to know its there if it happens.

Very happy with Gabrielle from SEIB. She has even taken the address where he has gone to – when I rang with all this information in April saying he was retiring the person I spoke to never mentioned the fact my premium would go down for a non ridden animal. I suppose I should have known really, its never happened before as I've never retired one and I never thought to push it.

I will definitely ring SEIB for a quote when I get my next horse. See if Gabrielle can work her magic again")

The lady said, ‘Oh we didn't realise he was retired, that will bring your premium down, and while we're here do you want to change his value so your premium will come down?”

So now he’s insured for destruction on humane grounds under BEVA guidelines, no vets fees. So now its £15 per month instead of £50 at a value of 4K! I have no idea how they determine value on a retired gelding but still. Stand more chance of getting that than 10K! I hope I never have to but nice to know its there if it happens.

Very happy with Gabrielle from SEIB. She has even taken the address where he has gone to – when I rang with all this information in April saying he was retiring the person I spoke to never mentioned the fact my premium would go down for a non ridden animal. I suppose I should have known really, its never happened before as I've never retired one and I never thought to push it.

I will definitely ring SEIB for a quote when I get my next horse. See if Gabrielle can work her magic again

.

.